Home Renovation Financing Options in Omaha: HELOC, Loans & What to Know

Understanding your financing options is the first step toward a stress-free renovation. Photo: LongView Renovation.

Most home renovations in Omaha cost between $25,000 and $100,000 or more, and very few homeowners write a single check to cover the entire project. That is not a sign of financial weakness. It is a sign of smart planning. The homeowners who get the best results are the ones who understand their financing options before they pick up a hammer or sign a contract.

Whether you are planning a kitchen overhaul, a basement finish-out, or a full exterior transformation, the way you pay for the work shapes everything from project scope to timeline to long-term cost. A poorly chosen loan can add thousands in unnecessary interest, while the right financing structure can actually improve your net return on investment.

This guide breaks down the five most common ways Omaha homeowners finance renovations in 2026, with current rate ranges, honest pros and cons, and practical advice on matching each option to the right type of project.

What You'll Learn:

- • How HELOCs, home equity loans, FHA 203(k), and personal loans compare for Omaha renovations

- • Current 2026 rate ranges and qualification requirements for each financing type

- • Tax benefits and Nebraska-specific incentives that reduce your effective borrowing cost

- • Red flags and financing traps to avoid when working with contractors

Home Equity Line of Credit (HELOC)

A HELOC works like a credit card secured by your home. Your lender approves a maximum credit line based on your home equity (typically up to 80-85% of your home's appraised value minus your existing mortgage balance), and you draw funds as needed during a set draw period, usually 5 to 10 years. You only pay interest on what you actually borrow, and you can draw, repay, and draw again throughout that period.

In the 2026 Omaha market, HELOC rates typically range from 7% to 9% variable, tied to the prime rate. Most Nebraska lenders offer HELOCs with no or low closing costs, making them one of the most accessible equity-based options.

Pros

- • Flexible draw schedule matches phased renovation timelines

- • Interest-only payments available during draw period

- • Interest may be tax-deductible if funds improve your primary residence

- • Low or no closing costs compared to home equity loans

Cons

- • Variable rate means payments can increase if prime rate rises

- • Your home serves as collateral, creating foreclosure risk if you default

- • Temptation to overborrow when credit line is readily available

- • Repayment period payments can spike when draw period ends

Best For:

Phased renovations where the total scope is uncertain, projects with multiple stages spread over months, and homeowners who want to draw only what they need as work progresses. Ideal for a kitchen remodel that might expand into a dining room reconfiguration, or an exterior project done in phases across two seasons.

Home Equity Loan

A home equity loan delivers a single lump sum at a fixed interest rate, repaid in equal monthly installments over a set term (typically 5 to 20 years). Think of it as a second mortgage with predictable payments from day one. Lenders in the Omaha market currently offer home equity loans in the 7% to 8.5% fixed range for borrowers with good credit.

The key difference from a HELOC is certainty. You know exactly what your payment will be every month for the life of the loan. That predictability makes budgeting straightforward, which is why home equity loans pair well with well-defined renovation projects where the scope and cost are locked in before construction begins.

Pros

- • Fixed rate means your payment never changes

- • Predictable monthly payments simplify household budgeting

- • Interest may be tax-deductible for home improvements

- • Higher borrowing limits than unsecured loans (up to $250K+)

Cons

- • Closing costs of 2-5% increase your effective borrowing cost

- • Less flexible than a HELOC if project scope changes

- • Home serves as collateral, same foreclosure risk as HELOC

- • Appraisal required, adding $300-$600 and 2-3 weeks to timeline

Best For:

Well-defined renovation projects with a known budget, such as a complete kitchen remodel with finalized plans, a bathroom renovation with selected materials, or a full roof replacement. If you have a signed contractor proposal with a fixed price, a home equity loan matches that structure perfectly.

FHA 203(k) Rehabilitation Loan

The FHA 203(k) is a government-backed mortgage that rolls your home purchase price and renovation costs into a single loan. It is specifically designed for buyers who want to purchase a home that needs work, renovate it, and finance the entire package with one closing, one monthly payment, and one set of closing costs.

There are two types. The Standard 203(k) covers major structural work, room additions, and renovations exceeding $35,000 with no upper limit beyond FHA loan limits for your county. The Limited 203(k) (formerly called Streamline) covers non-structural repairs under $35,000, such as kitchen updates, bathroom remodels, flooring, and painting.

Pros

- • Low down payment of just 3.5% (vs. 20% for conventional + renovation)

- • Single closing saves thousands in duplicate closing costs

- • Can finance structural repairs, additions, and major systems work

- • Available to borrowers with credit scores as low as 580

Cons

- • FHA mortgage insurance premium (MIP) adds to monthly cost

- • Contractors must be FHA-approved, limiting your options

- • Longer approval and closing timeline (60-90 days typical)

- • Standard 203(k) requires a HUD consultant, adding $400-$1,000

Best For:

Buyers purchasing a fixer-upper in Omaha who want to finance both the purchase and renovation in one package. Particularly valuable in Omaha's older neighborhoods like Dundee, Benson, and Midtown, where charming homes often need significant updates to mechanical systems, kitchens, and bathrooms.

Personal and Unsecured Home Improvement Loans

A personal loan for home improvement is an unsecured, fixed-term loan that does not require your home as collateral. You receive a lump sum, repay it in fixed monthly installments over 2 to 7 years, and your home is never at risk of foreclosure if you hit a financial rough patch. Rates in 2026 typically range from 8% to 15% depending on your credit score, debt-to-income ratio, and loan amount.

The trade-off is straightforward: higher interest rates in exchange for speed, simplicity, and the security of keeping your home off the table. Many Omaha homeowners use personal loans for smaller projects that do not justify the closing costs and timeline of equity-based financing.

Pros

- • Fast approval, often within 1-3 business days

- • No home appraisal, no closing costs, no lien on your property

- • Your home is not at risk if you default

- • Fixed rate and fixed payment for the life of the loan

Cons

- • Higher interest rates than equity-based options (8-15%)

- • Lower borrowing limits, typically maxing out around $50,000

- • Shorter repayment terms (2-7 years) mean higher monthly payments

- • Interest is not tax-deductible

Best For:

Smaller renovation projects under $25,000, homeowners with excellent credit who qualify for rates at the lower end of the range, and situations where you need funds quickly without the 3-6 week equity loan process. Common uses include bathroom refreshes, flooring replacement, interior painting, and single-room updates.

Contractor Payment Plans

Many reputable contractors, including LongView Renovation, offer structured payment plans tied directly to project milestones. This approach aligns your payments with tangible progress, so you are never paying ahead of completed work.

Milestone-based payment plans align your spending with verified progress on the job.

How LongView Structures Payments

Our standard payment structure breaks the total project cost into three milestone-based installments:

- Deposit (30-40%): Due at contract signing, covers material procurement and project mobilization

- Rough-in payment (30-35%): Due when framing, electrical, plumbing, and mechanical rough-ins are complete and inspected

- Completion payment (25-35%): Due at final walkthrough after punch list items are resolved

Key Advantages

- No interest charges: On short-term plans (projects under 3 months), there is no financing cost

- Built-in accountability: You only pay when verifiable milestones are reached

- Combinable: Pair a contractor payment plan with a HELOC or personal loan to manage cash flow

Tax Benefits of Renovation Financing

The right financing structure can unlock tax benefits that meaningfully reduce your effective cost of borrowing. Here are the three main categories relevant to Omaha homeowners in 2026:

Mortgage Interest Deduction

Interest paid on HELOCs and home equity loans is tax-deductible if the borrowed funds are used to "buy, build, or substantially improve" your primary residence. This deduction applies to up to $750,000 in total qualified mortgage debt. For a $50,000 home equity loan at 8%, that translates to roughly $4,000 in deductible interest in the first year, saving approximately $880-$1,200 depending on your tax bracket.

Energy Efficiency Tax Credits

The Inflation Reduction Act continues to provide significant credits in 2026 for energy-efficient home improvements:

- Heat pumps and HVAC: Up to $2,000 credit per year

- Insulation and air sealing: Up to $1,200 credit per year

- Energy-efficient windows and doors: Up to $600 per item (windows), $500 (doors)

- Electrical panel upgrade: Up to $600 credit (required for many energy upgrades)

Nebraska-Specific Incentives

- OPPD and MUD rebates: Omaha Public Power District and Metropolitan Utilities District offer rebates for high-efficiency furnaces, insulation upgrades, and smart thermostats

- Nebraska Energy Office: Dollar and Energy Saving Loans program offers below-market rates for qualifying energy improvements

- Property tax impact: While renovations may increase assessed value, Nebraska's homestead exemption and valuation caps can moderate the impact for primary residences

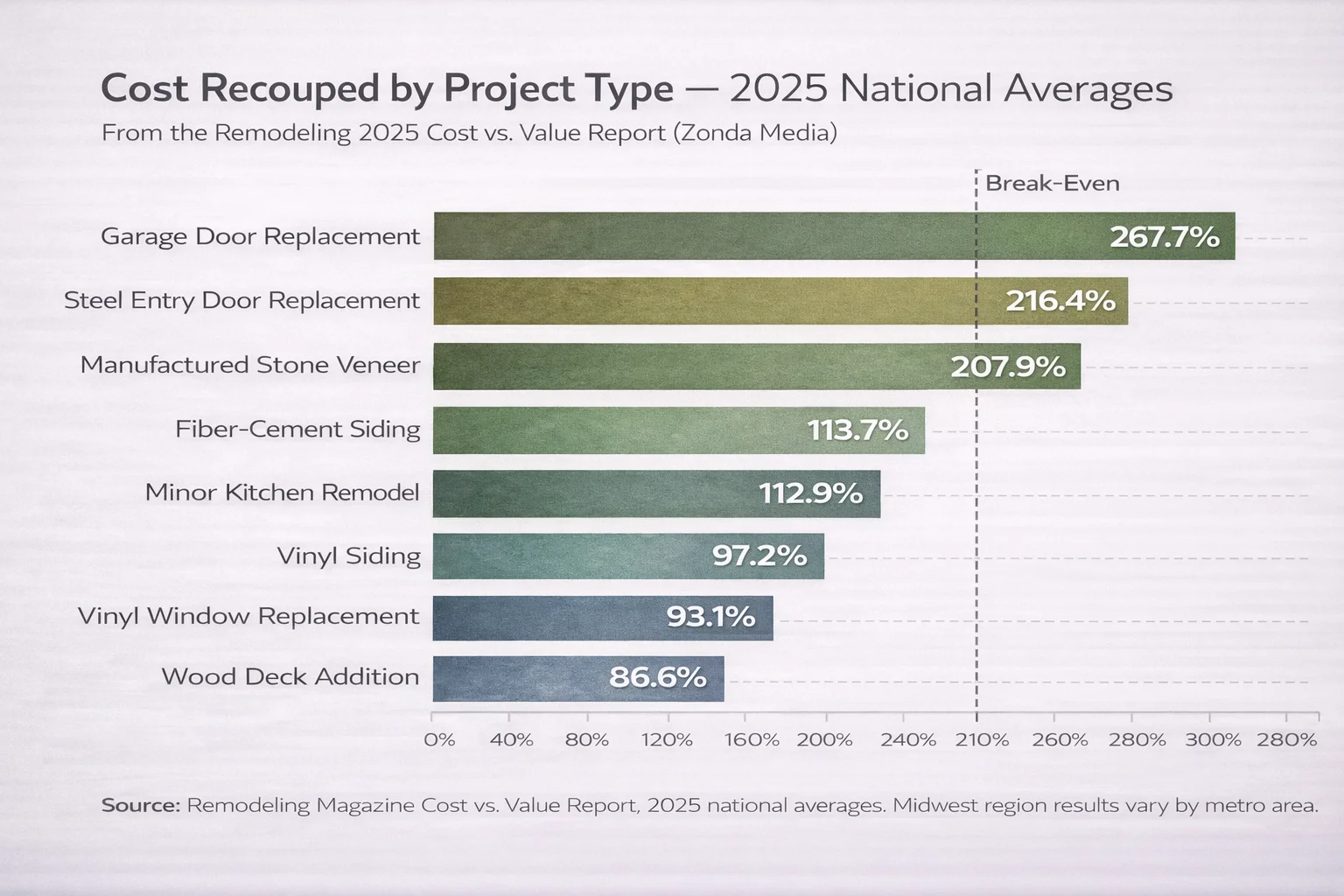

How to Calculate Your Renovation ROI Before Borrowing

Before you sign a loan agreement, run the numbers. Understanding your true cost of renovation, including financing charges, helps you decide whether borrowing makes sense and which option delivers the best net return.

Cost recouped by project type, 2025 national averages. Source: Remodeling 2025 Cost vs. Value Report (Zonda Media). Midwest region results vary by metro area.

Practical Example: $40,000 Kitchen Remodel

- • Project cost: $40,000

- • Value added to home: $32,000 (80% cost recouped — conservative estimate; the 2025 CVV Report shows minor kitchen remodels recouping 112.9% nationally, though Midwest results vary by metro area)

- • Financing method: Home equity loan at 7.5% fixed, 10-year term

- • Total interest paid over 10 years: approximately $16,700

- • Total cost of project with financing: $56,700

- • Net cost after value added: $56,700 - $32,000 = $24,700

- • Tax deduction value (est.): $3,700 in interest deductions at 22% bracket

- • Effective net cost: approximately $21,000 for 10 years of daily kitchen enjoyment

That $21,000 effective cost works out to roughly $175 per month for a kitchen you use every single day. When you frame it that way, financing a high-ROI renovation often makes more financial sense than sitting on deferred maintenance that quietly erodes your home's value.

Red Flags: Financing Traps to Avoid

Not all financing offers are created equal. Here are the warning signs that a deal is designed to benefit the lender or contractor more than you:

Contractor-Arranged Financing with Hidden Fees

Some contractors push in-house financing or "preferred lender" programs that include origination fees, dealer markups, or inflated rates bundled into the project cost. Always compare any contractor-recommended financing against rates you can get independently from your bank or credit union.

0% Introductory Rates That Balloon

Promotional 0% APR offers sound attractive, but read the fine print. Many carry deferred interest, meaning if you do not pay off the entire balance within the promotional period (often 12-18 months), you owe all the accrued interest retroactively, sometimes at rates of 20% or higher.

No-Documentation Loans

Any lender willing to approve you without verifying income or assets is charging a premium for that risk, and the terms rarely favor the borrower. Legitimate renovation financing involves documentation because responsible lending requires it.

Excessive Draw Schedules

Be cautious of contractors who demand 50% or more upfront before any work begins. Reputable contractors structure payments around milestones, not front-loaded draws. An excessive upfront payment puts you at risk if the contractor delays or fails to perform.

LongView Pro Tip

Get pre-approved for financing before your first contractor consultation. Knowing your approved amount sets a realistic scope from day one and prevents the disappointment of designing a $75,000 kitchen when your budget supports $45,000. Pre-approval also signals to contractors that you are a serious buyer, which typically gets you faster responses and more detailed proposals.

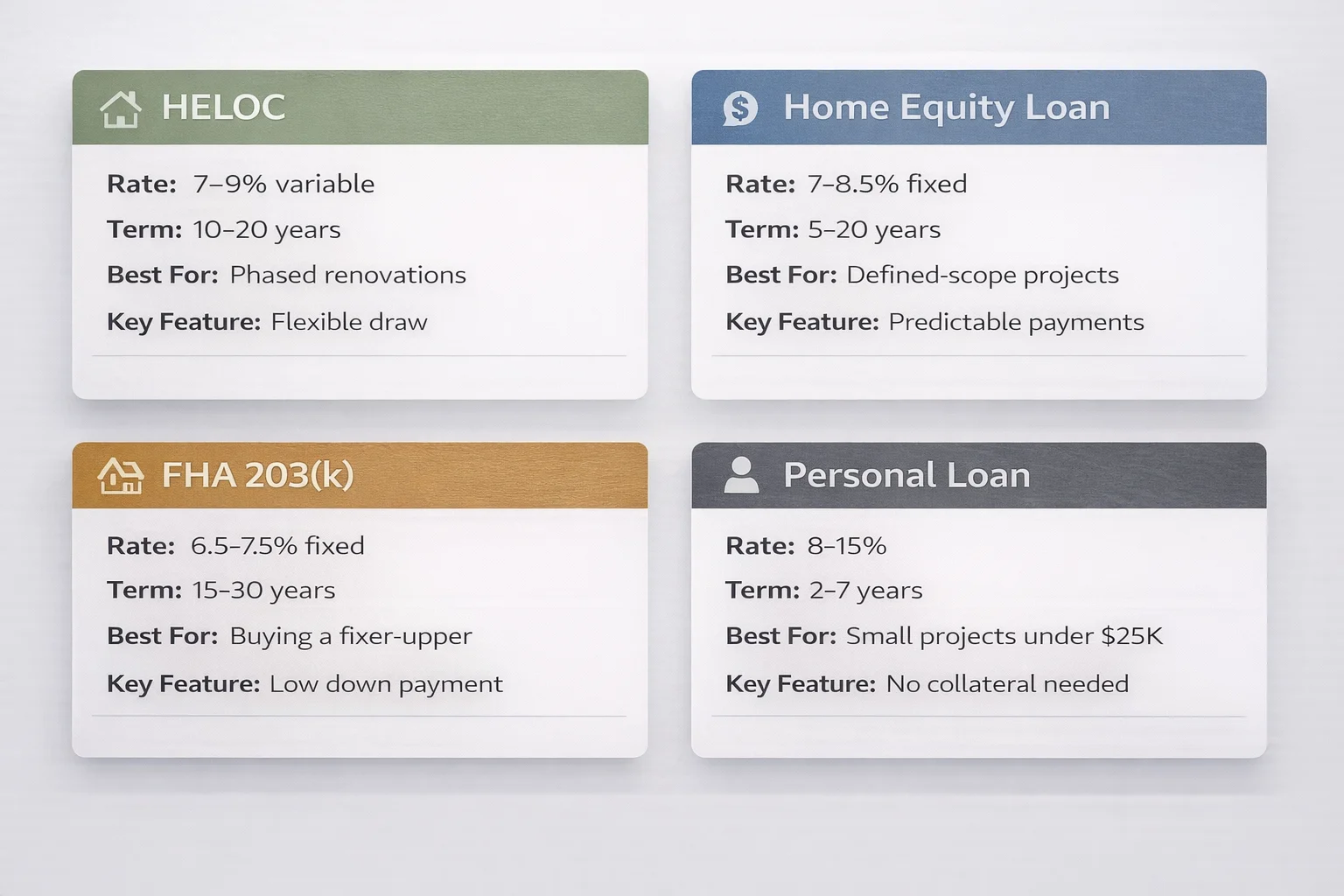

Financing Options at a Glance

Side-by-side comparison of renovation financing options available to Omaha homeowners in 2026.

HELOC

- Rate range: 7-9% variable

- Best for: Phased projects, uncertain scope

- Key consideration: Variable rate risk; budget for rate increases

Home Equity Loan

- Rate range: 7-8.5% fixed

- Best for: Defined-scope kitchen/bath, known budget

- Key consideration: Closing costs (2-5%) increase total cost

FHA 203(k)

- Rate range: Market mortgage rates + MIP

- Best for: Buying and renovating a fixer-upper

- Key consideration: FHA-approved contractors required; longer timeline

Personal Loan

- Rate range: 8-15% fixed

- Best for: Small projects under $25K, fast funding

- Key consideration: Higher rates; no tax deduction; no home risk

Know Your Budget. Start Your Project.

Free Consultation & Custom Quote

Once you understand your financing options, the next step is a clear project scope and an honest estimate. LongView Renovation provides transparent, line-item pricing so you can match your financing to a real number, not a guess.

Free Consultation

In-home project assessment

Project Scope

Defined plans and materials

Custom Quote

Transparent pricing breakdown

The Right Financing Makes the Right Renovation Possible

Financing is not the enemy of a smart renovation. It is often the enabler. The key is matching the financing structure to your project, your timeline, and your risk tolerance. A HELOC gives you flexibility for evolving projects. A home equity loan gives you certainty for defined scopes. An FHA 203(k) lets you buy and build in one move. A personal loan keeps things fast and simple for smaller work.

Whatever path you choose, start with clear numbers. Know what your renovation will cost, what value it will add, and what your monthly payment will be. When those three numbers make sense together, you can move forward with confidence.

LongView Renovation provides detailed, transparent estimates that give you the numbers you need to have a productive conversation with your lender. Whether your project is $15,000 or $150,000, the process starts with understanding what the work actually costs.